Predetermination: the Budget Built Without Asking

The government already knew the answer it wanted —and what that tells us about the state of the state

Australians are witnessing the confidence of a government that believes it already knows the answer, and so need not ask the question.

The 2026–27 Budget’s tax package—the largest restructuring of personal taxation since the Ralph Review of 1999—was handed down on 12 May in precisely that spirit. Seven interlocking measures reversing 27 years of capital gains architecture, a new minimum tax, a quarantine on negative gearing, and, almost as an aside, a 30 per cent minimum tax on discretionary trusts affecting hundreds of thousands of structures.1 Announced, effective, and—on every core design choice—consulted upon for a grand total of zero days before the decision was made.

This is not a column about whether the policy is right.2 Reasonable people hold that the capital gains discount distorts investment and that intergenerational asset inequality is a problem worth confronting. The argument here is narrower and, I think, more reflective of the type of nation we are becoming, and thus more deeply concerning: the manner in which this package was produced tells us something uncomfortable about the condition of the Australian state, and that the condition is worse than the headline numbers suggest.

Process is not a courtesy

It is fashionable to treat consultation as a matter of convenience, or bureaucratic throat-clearing—a delay between a good idea and its implementation, indulged by the timid.

This is backwards. Consultation, along with transparency and accountability, is how a government discovers what it does not know before it is too late to matter. Consultation is the mechanism by which the people who will actually operate inside a policy—the small business owner running a family trust, the self-funded retiree holding a pre-1985 asset, the founder whose entire stake is sweat equity with a zero-cost base—tell the state where its design will break.

When that mechanism is bypassed, the defects do not disappear. They simply surface later, more expensively, and in forums that cannot fix them.

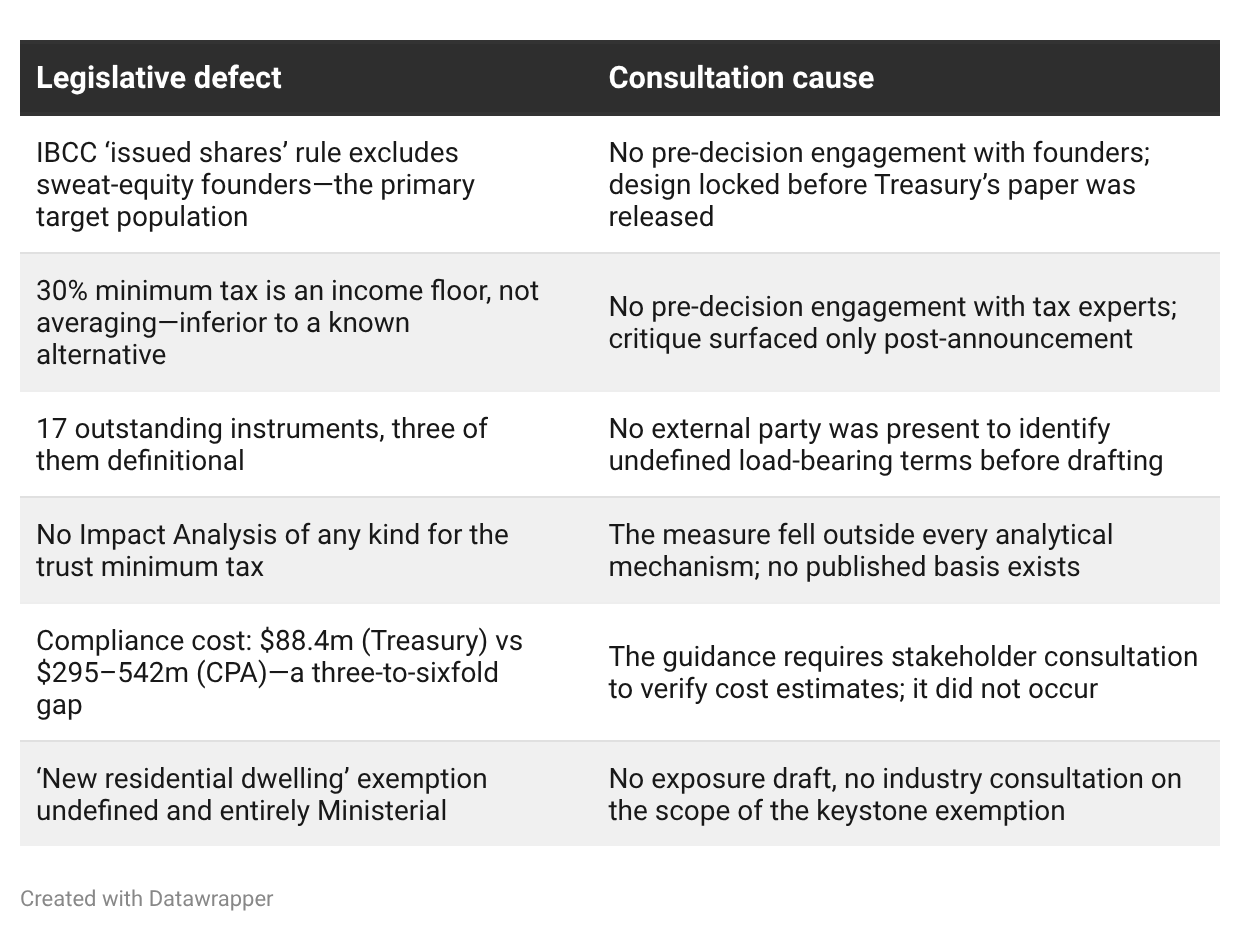

Consider the burdens and risks that are being transferred by the state on to different constituencies. The proposed Innovative Business CGT Concession, sold as relief for start-up founders, contains an ‘issued shares’ requirement that—by Treasury’s own admission on page four of its consultation paper (released post-hoc on 18 June)—may exclude the very founders it purports to help. The 30 per cent minimum tax on capital gains was described by the government as taxing gains ‘closer to the rate an individual faced during their working life.’ That is a description of income averaging.3 What was legislated is a flat floor, which is not averaging at all—a point made at Senate hearings by the e61 Institute, the Tax and Transfer Policy Institute, and Saul Eslake, none of whom oppose the reform’s direction. The package leaves 17 separate legislative instruments unmade, three of them definitional, without which the architecture simply does not function.

Parliament is being asked to approve a policy whose keystone terms—including the ‘new residential dwelling’ exemption on which the entire negative gearing supply argument rests—have not yet been written.

Each of these is not a defect that emerged despite good consultation. Each is a defect that consultation exists to prevent. The causal chain runs in one direction, and it is worth setting out plainly (if not exhaustively).

This is the anatomy of a policy assembled without the people who would have to live inside it.

The hypocrisy is the point

What elevates this from incompetence to something more corrosive is that the government already knows better—and has said so, in its own documents. Its own framework states that consulting affected groups is how you check the accuracy of your cost estimates. And ‘[w]hen a new policy is developed in isolation, without consultation, it is easy to think that it is no big deal and that the regulatory impact will not be significant.’

The Office of Impact Analysis’s own Best Practice Consultation guidance specifies a minimum of 30 days, and up to 60 is ‘usually appropriate’—with the caveat that the more significant and complex the proposal, as here, the longer the time frame that should be allowed. Departments should be aware of the burden on small business and allow for busy periods and holidays, extending time periods accordingly. Treasury’s own 2019 guidance on consulting small business demands early, open-minded engagement and explicitly prohibits consulting on a predetermined outcome.

Measured against the standards the state has written for itself, the package fails on every axis. Zero days consultation period where 30 is the basic requirement. A predetermined architecture dressed as open consultation. An annual compliance cost estimate that the professional bodies put at three to six times Treasury’s figure4—precisely the error that pre-decision engagement is designed to catch.

The government is not failing to meet some external ideal of good practice. It is failing to meet its own published rules, while invoking the language of consultation to legitimate decisions already taken.5 That is not an oversight. It is hypocrisy with a certification letter attached.

And the certification deserves a word of its own. The Impact Analysis Equivalent for the capital gains and negative gearing measures was signed by a Treasury deputy secretary on 11 May, acknowledged by the OIA the same day, and built partly from the Budget paper announcing the policy—the decision offered as evidence that the analysis behind the decision was sound. The discretionary trust minimum tax, affecting hundreds of thousands of structures, received no Impact Analysis at all. Not a deficient one. None.

What it says about the APS

I have spent enough years inside and around the Australian Public Service to know that this is not the work of careless individuals who may conveniently be hung out to dry.

This is the work of an institution that has quietly lost the standing, and perhaps the capacity, to insist. Frank and fearless advice is not a slogan; it is a professional obligation that requires an APS confident enough to tell a Treasurer and his office that the package is not ready, that the trust measure needs an analysis, that 30 days is the floor and there is a reason for it.

The accumulating evidence—the ANAO’s finding that OIA documentation met requirements in as few as a quarter of cases (paragraph 3.38), the Division 296 precedent of a two-week consultation window in 2023, and now this—does not describe a one-off lapse. It describes an erosion: of process discipline, of institutional independence, of the professional self-respect that lets officials hold a line under political pressure.

This is the governance debt that does not appear on any balance sheet. Each shortcut is individually survivable. Cumulatively, they hollow out the state’s ability to make hard decisions well—to weigh alternatives, absorb dissent, and produce policy that survives contact with reality.

Wilful deafness

A country with Australia’s strategic exposure cannot afford a state that has forgotten how to think before it acts. The cost of poor consultation is not merely worse tax law, though it is certainly that. It is a crippled economy and productivity foregone as founders and small businesses navigate a two-tier compliance economy. It is innovation deterred by a concession that may not reach the people it names.

That heedlessness means that trust—the quiet, load-bearing assumption that the state will follow its own rules and not act capriciously—is spent down a little further, on a Budget that asked no one. Omission, to focus on the perceived needs of some, harms all.

The Parliamentary Library has produced an exhaustive overview of the Bills and the response, as of 17 June: recommended reading. Parliamentary Library, Bills Digest No.67, 2025-26.

And let’s not forget how well that worked with Robodebt.

Potentially with what CPA Australia considers a likely ‘total one-off transitional valuation burden at between $675 million and $825 million, a figure that was not disclosed by Treasury’ for everyday collectables.

Moreover, such behaviour quickly becomes normalised, not least as the taxation changes will subsumed into part of everyday living, harder to protest, to disentangle and to reverse.