Senate Estimates Quick Brief – Day Seven

Thursday is the fiscal and structural heart of the entire two-week Estimates cycle.

Treasury in full—macroeconomic, markets, fiscal, and revenue—plus the RBA and ATO, appears before the Economics Committee across a fourteen-hour session. The analytical framework for this committee comes directly from ‘What Kind of Society and Economy Does This Budget Strive to Create?: the Budget perpetuates a consumption and distribution machine, not an investment and production machine, with an 8:1 ratio of social spending to productive investment, resting on productivity assumptions that have not been independently validated and cannot be delivered without state cooperation that has not been formally secured.

The Education and Employment Committee carries schools, curriculum, early childhood, and teaching quality—the long-run human capital question that the Budget’s productivity claims ultimately depend on.

Community Affairs carries Social Services—the $308.7 billion social security architecture, the NDIS cost trajectory, and the algorithmic welfare system.

FADT shifts to Foreign Affairs and Trade—the external face of the strategic insolvency argument.

Each committee has a meta-question today. Australia’s external strategic posture—AUKUS, Pacific engagement, the Quad, the China stabilisation—makes implicit assumptions about domestic cohesion, institutional credibility, and the public’s willingness to sustain strategic costs over generational timescales. Those assumptions depend on a population with reasonable confidence in its institutions, a productive and complex, capable economy, a social safety net that absorbs the cost-of-living shocks now operating without producing the marginalisation the AFP Commissioner identified as a radicalisation precursor, and fiscal assumptions that are honest with Parliament about what can realistically be delivered.

The Budget has made a specific bet about where Australia is going and what it will cost. Each committee today should address the veracity and strength of the assumptions underlying the Budget over the long-term.

Last, the standing strategic questions, operational questions for senior executives, and the QON/NFP/DTBNYA accountability framework from last week remain live.

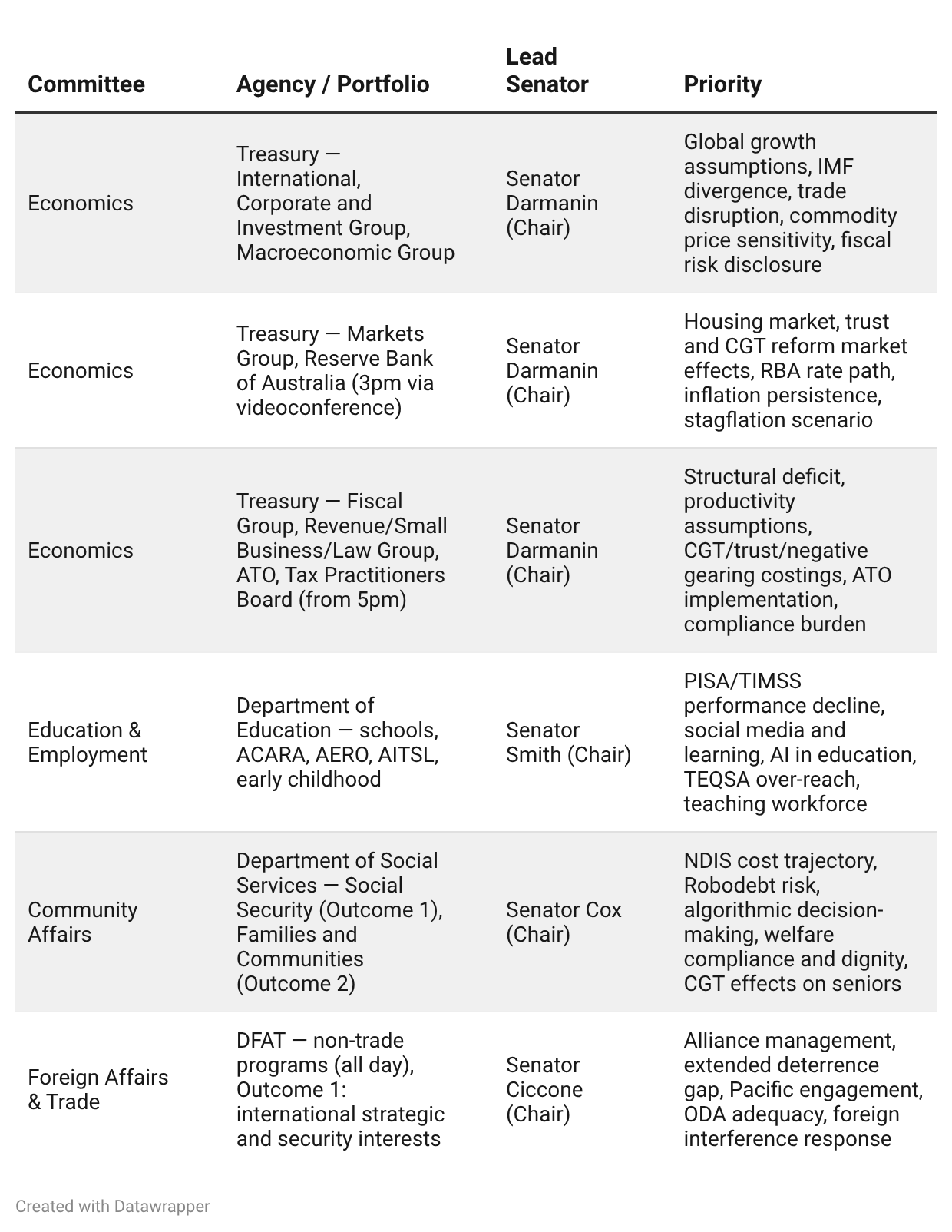

Thursday 4 June — Committee Schedule

COMMITTEE 1 | Economics

Treasury (Macroeconomic Group (morning) and Markets Group (afternoon); RBA (afternoon)

Strategic Context

The analytical spine for Thursday’s Treasury session is the article ‘What Kind of Society and Economy Does This Budget Strive to Create?’ The Budget’s entire fiscal path—the return to surplus in 2034-35, the $150.5 billion four-year deficit—rests on productivity assumptions of $10.2 billion per year from regulatory reform and $13 billion from NCP gains, on commodity price forecasts at historically elevated levels, and on NDIS savings that require growth to fall from 21 per cent to 3 per cent annually. None of these has been independently validated. The IMF’s April 2026 World Economic Outlook downgraded global growth in direct response to trade disruption. Thursday is the only session in the Estimates cycle where Treasury’s macroeconomic assumptions, fiscal risk disclosure, and behavioural response modelling can be tested directly.

The meta question for the entire Treasury session follows from the article’s synthesis: this Budget is attempting to fund an increasingly expensive welfare state from an economy whose most productive members it is simultaneously giving less reason to stay, less support to build with, and fewer tools to accumulate wealth through. Whether that model is fiscally sustainable depends entirely on productivity assumptions that Treasury owns and Parliament has never adequately tested.

Priority Lines — Macroeconomic Group

Fiscal assumptions versus IMF divergence. The IMF’s April 2026 World Economic Outlook downgraded global growth in direct response to trade disruption from US tariff policy and the Hormuz closure. Australia’s Budget was handed down after that downgrade.

What is the specific divergence between the Budget’s global growth assumptions and the IMF’s April 2026 baseline—by year across the forward estimates? And for each percentage point of divergence in global growth: what is the estimated first-order impact on Australian commodity export revenues, on tax receipts, and on the structural deficit trajectory? If Treasury has modelled that sensitivity, it should be published. If it has not, why not?

What specific economic impact from the Hormuz closure is embedded in the Budget’s GDP growth, inflation, and revenue projections—and on what assumption about the duration of the closure are those forecasts based? If the forecasts assume closure resolution within a specific timeframe, what is that timeframe—and what is the forecast deviation if the closure persists for 12 months beyond that assumption?