Senate Estimates : Quick Brief—Day 8

Friday is the closing day of the two-week Estimates cycle and carries the regulatory architecture that sits underneath the Budget’s productive investment claim.

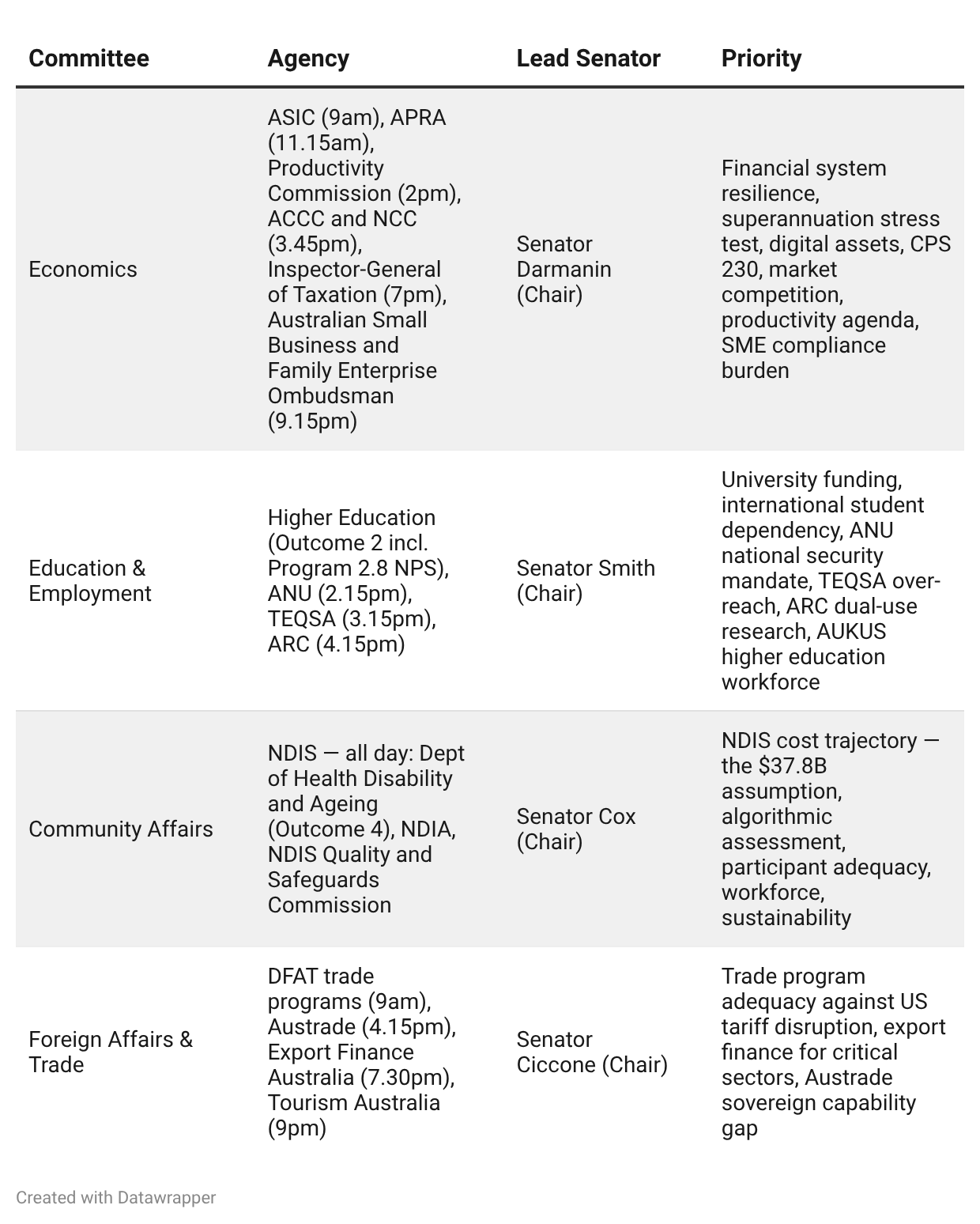

Friday 5 June 2026 | Economics (ASIC, APRA, Productivity Commission, ACCC, Small Business Ombudsman); Education (Higher Education, ANU, TEQSA, ARC); Community Affairs (NDIS); FADT (Trade)

ASIC, APRA, the Productivity Commission, and the ACCC are the institutions that shape the conditions under which private capital forms, deploys, and either builds complexity or extracts rent. The Small Business and Family Enterprise Ombudsman sits at the end of the Economics schedule—the most direct voice for the sector the Budget simultaneously relies on for growth and burdens with compliance.

In Education, Senators will address Higher Education, the ANU’s national security research mandate, the ARC’s dual-use research framework, TEQSA’s innovation-suppressing regulatory posture, and Education Program 2.8, the Higher Education NPS contribution—another AUKUS workforce line that mirrors DEWR’s Program 2.3.

Community Affairs carries the NDIS for the full day—the single most important fiscal assumption in the Budget, questioned for the first time in full.

FADT concludes with trade programs, Austrade, and Export Finance Australia—the external economic instruments of the strategic insolvency argument.

The IAT/algorithmic welfare finding from last week’s aged care session should now be carried explicitly into both the NDIS and ASIC data-governance questions. Friday is also the day most senators are running on reduced attention and committee rooms are thinning.

Friday 5 June — Committee Schedule

COMMITTEE 1 | Economics

Australian Securities and Investments Commission — Senator Darmanin (Chair)

Appearance: Friday 5 June, 9.00am–11.00am

Strategic Context

ASIC is the conduct regulator for financial markets and consumer financial services. Three threads from across the week converge here.

First, the Budget’s trust and CGT reforms will generate compliance and enforcement questions for ASIC—the behavioural response to closing trust structures will include restructuring activity that ASIC must monitor for compliance with the new rules.

Second, the digital assets framework—the Corporations Amendment (Digital Assets Framework) Bill 2025—extends ASIC’s licensing regime to digital asset platforms from 30 June 2026. The no-action period ends at precisely the moment this Estimates session is taking place.

Third, the IAT finding from last week’s aged care session connects here: ASIC oversees financial product disclosure and automated decision-making in financial services under the design and distribution obligations, and the same question about unaudited algorithms making consequential decisions applies to the financial services sector.

Priority Lines

Trust and CGT reform compliance. The Budget’s trust minimum tax and CGT discount replacement will drive restructuring activity across the trust and property investment sector before the measures take effect. Restructuring that is motivated by tax minimisation rather than genuine commercial purpose falls within ASIC’s general conduct jurisdiction.

Has ASIC developed a compliance and surveillance framework for the restructuring activity expected before the trust and CGT measures take effect—and is ASIC coordinating with the ATO on identifying restructuring that may constitute a scheme for the purposes of Part IVA?

ASIC and automated decision-making. The Community Affairs Committee heard last week that the Integrated Assessment Tool used to assess aged care entitlements was deployed without consultation on the final algorithm and without independent audit. The design and distribution obligations ASIC administers require product issuers to consider the likely outcomes for consumers—in effect, an obligation to understand what the product does and to whom.

Does ASIC have a current assessment of whether financial product issuers using algorithmic or AI-assisted product recommendation, credit assessment, or insurance pricing tools have validated those tools adequately—and has ASIC identified any cases where an algorithmic tool is producing outcomes for consumers that the issuer cannot adequately explain or audit?

Australian Prudential Regulation Authority

Appearance: Friday 5 June, 11.15am–1.00pm

Strategic Context

APRA’s May 2026 System Risk Outlook—published two weeks ago—is the most current independent assessment of Australia’s financial system resilience available at this Estimates. Its findings are directly relevant to the Hormuz and stagflation scenarios developed across the week. Phase 1 of APRA’s inaugural system stress test found that superannuation funds can continue to be a stabilising force during a shock, but in some cases their actions can amplify the negative effect on members and the broader system. CPS 230 operational resilience came into effect on 1 July 2025. And APRA has reinforced expectations around unlisted asset valuation governance—directly relevant to the Future Fund.

Priority Lines

The system stress test and Hormuz. APRA’s Phase 1 system stress test scenario assessed the impact of a significant financial market disruption alongside a major operational risk event. Phase 2 results are due mid-2026. The Hormuz closure—driving simultaneous supply-side inflation and demand compression—is precisely the kind of external shock that could trigger the financial market disruption component of that scenario.

Does the Phase 2 stress test scenario include an external supply-side shock—commodity price disruption, freight repricing, input cost inflation—of the kind the Hormuz closure represents?

Phase 1 found super funds can amplify negative shocks in some cases. What specific fund behaviours in a Hormuz-type scenario would amplify the shock—and what supervisory guidance has APRA issued to funds to mitigate that amplification risk?

CPS 230 compliance. CPS 230 requires all APRA-regulated entities to have operational risk management frameworks in place from 1 July 2025. APRA has stated its initial compliance focus is on larger entities.

What proportion of APRA-regulated entities have completed their CPS 230 implementation—and of those assessed to date, what proportion are fully compliant versus partially compliant?

Cyber security: 78 per cent of Commonwealth entities have not achieved Essential Eight Maturity Level 2. APRA-regulated entities—banks, superannuation funds, insurers—operate outside that framework but face equivalent cyber threats. Is APRA satisfied that the cyber resilience uplift among its regulated population is adequate against the threat environment ASIO and ASD have publicly described?

Unlisted asset valuation — the private credit risk. APRA has reinforced valuation governance expectations for superannuation funds investing in unlisted assets—private equity, private credit, infrastructure. A shift to alternatives has increased structural illiquidity and mark-to-model valuation dependence, including for superannuation funds with significant unlisted asset allocations.

Has APRA identified any superannuation funds whose unlisted asset valuations it considers potentially materially misstated—and what is APRA’s current assessment of the aggregate mark-to-market versus mark-to-model gap across the superannuation system’s unlisted asset holdings?

Productivity Commission

The Productivity Commission is the institution most directly responsible for the analytical foundation of the Budget’s $10.2 billion regulatory reform claim and the $13 billion NCP productivity gains. Those figures have been queried across multiple sessions this week without a satisfactory answer from Treasury or PM&C. The Commission is the appropriate place to close the loop.

PC — Budget-related modelling. The Budget’s return to surplus depends on $10.2 billion per year in regulatory reform savings and $13 billion in NCP gains. These figures have been attributed to Productivity Commission analysis across multiple Estimates sessions this week.

Can the Commission confirm: did it produce the modelling that underpins those specific figures, on what assumptions, using what methodology, and with what confidence interval around the central estimate? And does the Commission consider those figures achievable without formal state government legislative commitments—which have not been secured?

Australian Competition and Consumer Commission (ACCC)

Data and digital markets — the competition architecture. The ACCC’s Digital Platform Services inquiries have produced five reports over five years. The government’s response has been incremental. Meanwhile, the Budget’s digital productivity assumptions depend on competitive digital markets producing efficiency gains that concentrated markets cannot deliver. The VSA6 Microsoft lock-in and the DTA’s AI vendor relationships represent exactly the kind of digital market concentration the ACCC has been documenting.

Has the ACCC assessed whether the Commonwealth’s own whole-of-government ICT and AI procurement practices—specifically the VSA6 and the DTA’s AI framework—are consistent with the competitive market principles the ACCC promotes for the private sector?

The Budget’s NCP productivity gains depend partly on platform and digital market competition. What is the ACCC’s current assessment of whether Australian digital markets are becoming more or less competitive—and is the trend consistent with the $13 billion NCP productivity assumption?

The meta question. The Budget’s productive investment claim rests on regulatory reform and competition policy gains that require the ACCC to be adequately resourced, operationally independent, and sufficiently empowered to address the concentrated market structures that block productivity.

Is the ACCC satisfied that its current mandate, powers, and resourcing are adequate to deliver the competition policy conditions the Budget’s $13 billion NCP productivity claim requires?

Small Business and Family Enterprise Ombudsman

The Ombudsman’s function is to advocate for small businesses navigating Commonwealth regulatory and legal frameworks. The Budget adds compliance costs through IR measures, trust closure, CGT reform, and ATO systems changes simultaneously. The Ombudsman appears at the end of a 14 hour committee day in which Treasury, the ATO, and DEWR have each been asked about cumulative compliance burden without producing an aggregate assessment.

Can the Ombudsman confirm: has the Office conducted, or does it intend to conduct, a cumulative compliance cost assessment for small businesses under $10 million turnover covering all Commonwealth regulatory changes since 2022—and if not, who in government is responsible for that assessment, and why hasn’t it been done?