Senate Estimates: Quick Brief—Day Two

A focus on accountability.

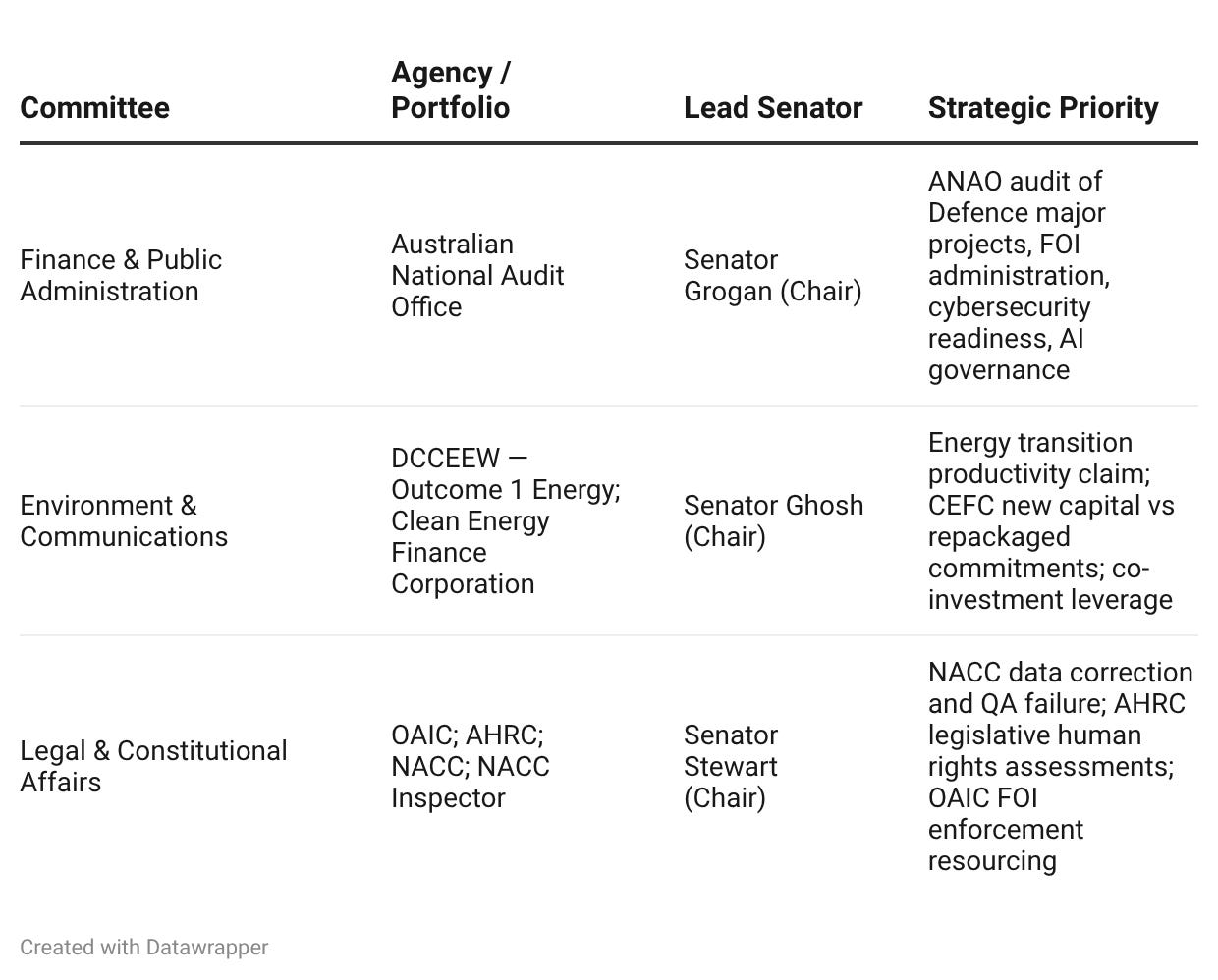

Our focus at Dead Reckoning is on democracy, governance, Australia’s strategic position, economic competitiveness and emerging technology, and that shapes our view of Senate Estimates. Day 2 picks up where Day 1 left the standing themes: fiscal assumptions, transparency classification, and the strategic gap between what the Budget promises and what it funds to completion. This brief covers the agencies of greatest accountability interest on Tuesday 26 May: the Australian National Audit Office (Finance & Public Administration Committee); the Clean Energy Finance Corporation and DCCEEW Energy Outcome (Environment & Communications Committee); and the Office of the Australian Information Commissioner, Australian Human Rights Commission, National Anti-Corruption Commission, and NACC Inspector (Legal & Constitutional Affairs Committee). The Series Primer — covering what Estimates is, why it matters, and where it fails — is in Brief #5 and is not repeated here.

The standing strategic questions, operational questions for senior executives, and the QON/NFP/DTBNYA accountability framework from Brief #5 remain live across the full two-week period.

Tuesday 26 May—Committee Schedule

COMMITTEE 1 | Finance and Public Administration

Australian National Audit Office — Senator Grogan (Chair), Senator Sharma (Deputy Chair)

Appearance: Tuesday 26 May, 4.15pm

Strategic Context

The ANAO is the Budget’s only independent auditor. Its three program areas—Financial Statements Audit, Performance Audit, and Performance Statements Audit—are not abstract governance machinery. They are the mechanism by which Parliament can know whether what departments say they are doing corresponds to what they are actually doing. On Tuesday, the ANAO’s current and recent audit program carries direct bearing on four of the Budget’s most important—and most vulnerable—assumptions.

Priority Lines of Inquiry

ANAO independence. The ANAO’s budget has been subject to real-terms constraint across multiple years. If the ANAO’s performance audit program cannot be maintained at its current scope, which audit areas—Defence, cybersecurity, AI, FOI—are at greatest risk of being deprioritised, and what is the accountability cost of that deprioritisation?

Defence major projects. The ANAO’s Major Projects Report has been discontinued. Of the 21 projects it last covered, Defence withheld Final Operational Capability dates for 19 of them on the ground that disclosure would damage security. Can the Auditor-General confirm:

first, whether the ANAO accepted that classification without independent assessment of the security claim;

second, whether the ANAO sought a legal opinion on whether the Vice Chief of the Defence Force has the authority to direct what the ANAO may publish; and

third, what alternative mechanism—if any—the ANAO now proposes to give Parliament independent visibility of cost-to-complete and schedule performance across $209 billion in Defence acquisition?

Submarines. The ANAO recently tabled an audit of the Collins Class Life of Type Extension program. That program is the single most important near-term capability commitment in the 2026 National Defence Strategy—without it, Australia has no viable submarine capability for the period between now and SSN delivery. Can the ANAO confirm:

what were the key findings on cost-to-complete and schedule, what recommendations were made, and has Defence accepted them in full?

given that this is precisely the category of project previously reported in the Major Projects Report—how does the ANAO propose to give Parliament ongoing independent visibility of this program’s performance?

ANAO independence under budget pressure: What is the ANAO’s current approved budget for 2026–27, how does it compare to the prior year in real terms, and is it sufficient to maintain the current scope of the performance audit program?

Has any agency sought to limit the scope of an ANAO performance audit in the past 24 months?

The JCPAA has publicly called for the ANAO to be exempted from the efficiency dividend.

In real terms — adjusted for CPI and the APS remuneration uplift—does the 2026-27 budget allow the ANAO to maintain its current performance audit program at the same scope and frequency as 2023–24?

If not, which audit areas have been reduced or deferred, and what is the dollar value of audit work that was requested or planned but not resourced to proceed?

FOI administration audit: The ANAO has previously audited the administration of the Freedom of Information Act across Commonwealth agencies—covered in the AGD appearnce on 25 May 2026; the OAIC will have also appeared earlier at 9am.

The systematic use of NFP and DTBNYA classifications documented in Brief #5—including $958.8 million in unexplained DTBNYA funds at the November 2024 Finance & Administration Committee—is the kind of pattern an ANAO performance audit is designed to test. If no such audit is currently scheduled, that absence is itself a question.

Can the Auditor-General confirm: is there a current or planned ANAO performance audit examining the administration of FOI exemptions across Commonwealth agencies, with specific attention to the use of section 33 (national security) and section 47 (commercial) exemptions?

If not—given that the NFP and DTBNYA classification pattern in the 2026–27 Budget papers represents a systematic restriction on parliamentary scrutiny of $958.8 million in public expenditure documented at the November 2024 Finance and Administration Committee—what would trigger one?